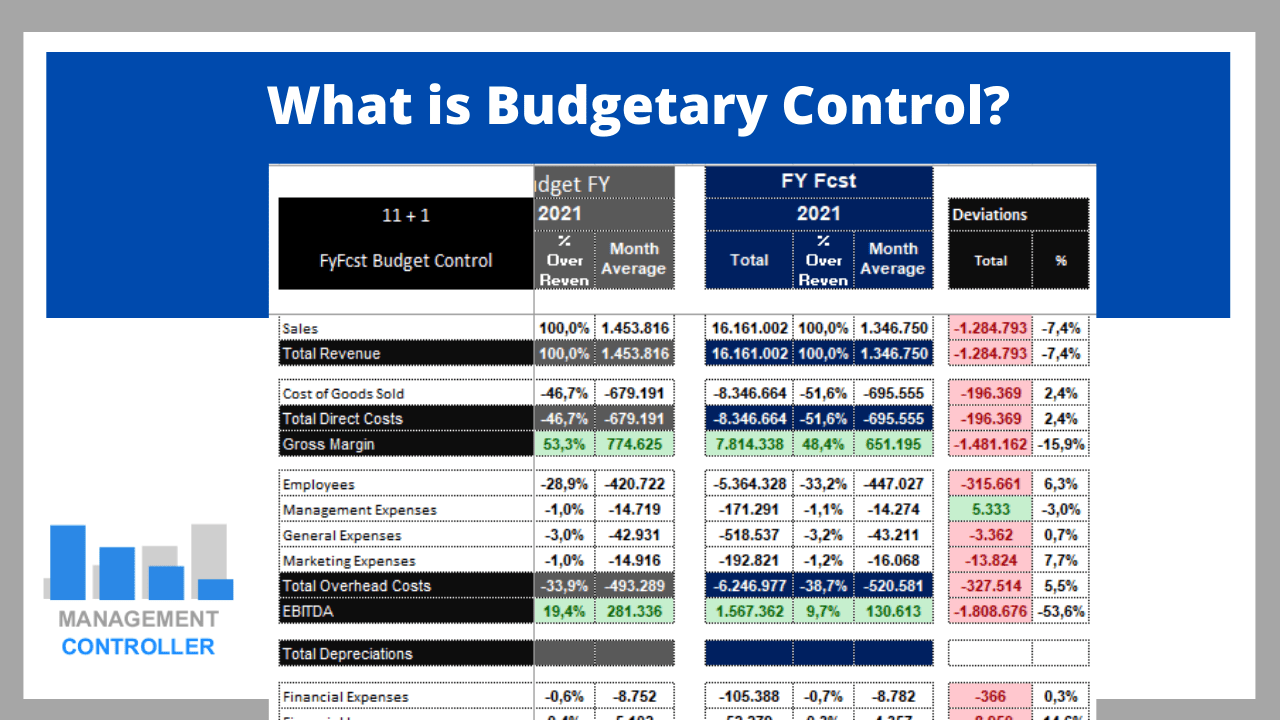

What is Budgetary Control.

Budgets are a very useful management tool. A budget is a management methodology to translate the company’s strategic objectives into financial approaches.

The usual objective of the company is to obtain sufficient and stable profits to satisfy both the shareholders and the workers.

And at the same time to generate enough liquidity for the company to balance the financial level.

The budget usually has an annual periodicity, thus coinciding with the fiscal year or financial year.

This means that the budget is sustainable and stable, regardless of its fluctuations or interannual variability, what is important is the constancy it generates.

This periodicity promotes continuous improvement and therefore competitiveness, that is, if we improve our results by a percentage every year, in the long term we will have achieved incredible results.

Without this periodicity, we cannot analyze or control the improvement of results, so we cannot ensure that in the long term the company is as competitive as its sector requires.

The continuous improvement promoted by the budget unconsciously or naturally implies constant growth. This growth makes it easier to survive, maintain market share, or even gain a larger share.

It can be argued that Budget Control keeps the company moving forward.

If the company has external shareholders, they will expect an average return for a minimum period of time, if this return is not achieved there is a good chance that the project will be abandoned.

An advantage for the company’s employees is that the Budget promotes motivation when it comes to achieving objectives. Not only from the economic point of view, but also from the assessment and performance of the work done.

A profitable company not only benefits shareholders, suppliers, employees, and public administrations through the payment of taxes. It can also bring benefits and advantages to society.

This reciprocal benefit automatically generates its own demand, which is fed back into the same company.

Budget Control is not a police control methodology, nor even pressure.

On the contrary, the budget is a reference to follow to achieve an objective.

The budget is drawn up to know where we have to go.

Does this mean that the budget can change? The budget does not change since we cannot modify the objectives each month to our convenience. The budget is generally related to the strategic plan, so its establishment and subsequent achievement is a strategic issue.

In many posts I read that the budget must be adjusted according to external o internal situations. This should not be like that. For certain reasons, a company can make small adjustments to the budget, but without affecting the established strategic line too much, and they are normally made at the beginning of the fiscal year or financial year.

In a way, the budget is immovable.

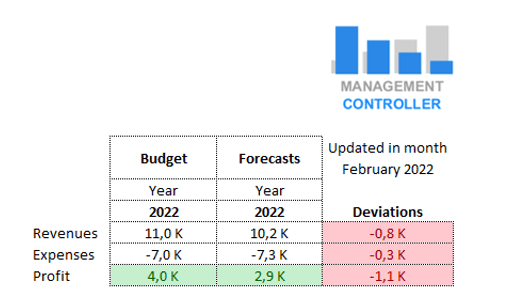

What the authors who try to justify changes in the budget throughout the year do not take into account is that a key element for budget management are the projections.

Projections of course are changing. They always change.

Projections at the beginning of the year are not the same as mid-year or end-of-year.

The projections are subject to changes in the sector, in the market, in actions of the competition, in circumstantial changes and in actions or decisions taken by the company to change the direction of the result.

For example, if the projections from February indicate that the company will have losses at the end of the year, the company has 10 months to take the necessary measures and convert these projected losses into profits.

Logical, right? If we know in advance that we are going to have losses, it would be incomprehensible to stand still and do nothing. Normally, this information motivates the company to move (hence the meaning of the word motivation)

The company will have to think about what measures to take to reverse the situation, otherwise, if the company does nothing and assumes the losses, not only will it have been a useless year, but it may have negative long-term implications.

To learn more about Budget Control models with Projections management, click here.

Some authors affirm that it is not necessary to comply with the budget, approaching it is enough. This depends on the company. In highly competitive sectors and with a budget closely linked to the strategic plan, compliance with it is essential for the survival of the company. For this reason, in sectors such as the automobile sector, compliance with the budget is essential for their strategic interests, both in the short and long term. Failure to not accomplish the budget could have serious consequences for the company’s competitiveness.

It is true that budget management should not be extremely detailed or complex, but this happens with any Management Control tool or methodology. The benefit of your application should always be greater than the costs of its implementation and maintenance.

How many reports are generated in companies that are very laborious in workers’ time and do not add great value to the company?

The degree of detail of the budget will be determined by the benefit that it contributes to it.

If the degree of detail is at the product, supplier or employee level, and this brings better results to the company, then it is worth it.

Many companies complicate their lives when preparing a budget, and for that reason they never get to start it.

These companies do not realize that they have all the information they need for their preparation in front of their PC screen.

The simplest information when starting up a Budgetary Control system is the accounting information.

After all, accounting is a reflection of what the company has been through in the past. Accounting, in addition to valuing assets and their respective depreciation, controlling debt and balances of customers and suppliers, also records revenues and expenses.

And this is what interests us, revenues and expenses, which difference is the profit or loss. simple, right?

The revenue is generated by the regular sales of the company. So if we set a sales target this will translate into accounting revenue. There may also be financial or extraordinary income, but they are generally not linked to the normal activity of the company.

We also have controlled expenses. Depending on the type of activity of the company, we can surely classify expenses as direct and overhead, or variable and fixed.

The normal thing is to know what kind of expenses we have, including which suppliers generate them.

We can also know what kind of personnel expenses we have, including depreciation, financial expenses, extraordinary expenses…

Everything is in the accounting, so if it is not falsified or manipulated, it is the best source of information and the simplest we have as a starting point to prepare a budget.

Is it necessary to make a detailed list of products with their respective sales projections in units and prices per month?

Or maybe we can take advantage of the accounting information from previous months and together with the commercial team determine a growth or reduction objective for the next year?

And the same with the rest of the accounting items.

It is not necessary to complicate your life to prepare a budget.

If, for example, we know that the main supplier is going to make us a price reduction of 5%, which represents 45% of the costs of raw materials, and we have the objective of increasing sales by 7%, then we can apply a formula for calculate what the spending goal of this supplier is going to be. In most cases it is not necessary to go to an excessive degree of detail.

Another example could be that the rental of the warehouse is going to increase by 3% per contract. Or that we have to adjust the payroll of employees according to the sector agreement.

All this information will allow us to build a budget in a simple way without having to generate complex predictive algorithms.

Once a budget has been prepared in line with the strategic plan and SMART (since it is an objective), the most important thing, as I have mentioned before, is knowing how to manage projections.

Normally the budget for the following year is prepared before the end of the current year. It doesn’t make sense to set a budget in March when the fiscal year ends in December.

As I have mentioned, the budget is an objective, but the projections are what is really going to happen.

Imagine that we have set the goal and suddenly in March a virus appears out of nowhere that generates a pandemic and modifies all plans. This has been a reality.

Companies have had to adapt to the new situation. Those companies that have done a good job adjusting the projections and have taken the necessary measures based on the projections will surely have been able to finish the year well.

But how do we know if the projections are going to be fulfilled?

The projections are not set in stone, they change every month, therefore they are adjusted according to the scenario and the actions taken.

The closer we get to the end of the fiscal or financial year, the more accurate they will be and the less room for error there will be.

Do you still have doubts about how to set up a Budget Control System?

Click here to see an example of a real Budget Control, a methodology implemented in many companies.

If you need more information, contact me.

Download a DEMO of the 2kM15 version Budget Control.

Download Budget Control Ytd FyFcst M15 Example of Budgetary Control Reports

J.A.T

This way of keeping a budget control changes everything. We had never tried it because we did not think it would be useful. But with Dani’s methodology we now see the potential and we think it will help us in very many ways.

R.M

The Budgetary Control technique and tool is helping us to better manage expenses and that allows us to make better decisions. A great contribution to our management control.

Contact for more information

ContactMore information about Controlling Excel Tools

- Personal Finance Free Excel Template

- Projects Costs Calculation and Control M3 Excel Template

- Inventory Control and Dashboard Excel Template

- Employee Absences Free Excel Template

- Budget Control Excel Year-to-Date & Full-Year Forecast M11

- Employee Management Free Excel Download

- KPI OEE Report Excel Free Template

- Planning Purchase Orders Excel report with ODOO data

- Cash Flow Control M1 Free Excel Template

- Human Resources HR Budget Excel Template

- Timesheet Control and Report Free Excel Template

- Digital Marketing Dashboard Control M1 Free Excel Template

- Excel Budget BOM Manufacturing Costs and Margins M15

- Excel Template Cash Flow Forecast M15

- Excel spreadsheet Strategic Plan

- Download Example of Excel thermometer chart

- Excel Template Financial KPIs Dashboard

- Retail Commerce Profit Analysis Free Excel Template

- What is Contract Management Excel Template and download a spreadsheet

- What are the benefits of a Budgetary Control System

- How to calculate costs in a Company

- Payments Due Date Control Free Excel Template

More Videos about Management Accounting

![]()

Industrial company financial manager

Dani is helping us to use ODOO more efficiently, we are rapidly leveling up with the ERP. It is also preparing us very useful analysis and control reports and outstanding management tools. Always available by phone or email, willing to help and collaborate in everything that is proposed. Very professional and fast work. A key service for our company.

Controlling Consultant

Controller ODOO ERP

Email: dani@cashtrainers.com