What are the benefits of a Budgetary Control System.

A financial budget is nothing more than an objective that the company sets in economic terms of how it wants or needs the result to be for a certain period.

The financial objective or budget must be aligned with the strategic plan of the company.

If the company has a growth plan, the financial objective must be in line with the expected growth (more hires, greater investment in advertising and marketing, investment in capacity of production…)

However, if the company has an adjustment plan due to the drop in demand, the objective should be related to this plan; personal cuts, investment stoppage, reduction of fixed expenses…

So the budget is our goal at an economic level regarding what the company plans to do and therefore the result it hopes to achieve.

This has several advantages over not having a budget and not keeping track.

If the company does not have a goal, the company can give one result or another, the result will be uncertain.

If the result is not controlled from the beginning, the company cannot establish a plan of measures to achieve it or apply corrective measures to modify the trend of a deviation from the real one with respect to the objective.

If the company does not set a goal, it does not know where it wants to go, it is like driving a car without having a destination in mind, we simply drive until at a given moment the vehicle runs out of fuel.

If we set an income objective and an expense objective, we have 2 control options.

1) Accumulated control as the accounting is closed each month (Year-to-Date or Accumulated to date).

This gives us a vision of how we are going to date with respect to the objective, if we are going well or we are doing badly, if we are going badly we can plan actions to correct the situation, however we do not have a perspective of how we are going until the end of the year with respect to the budget.

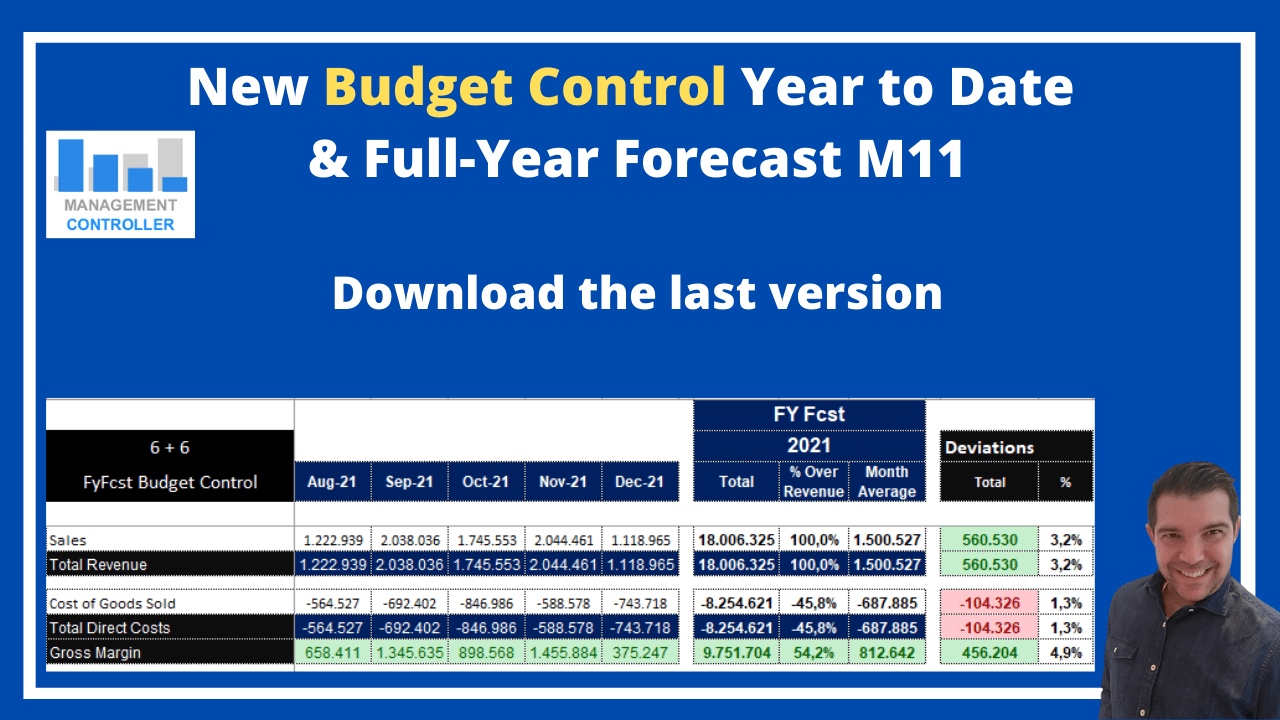

2) Control Full-Year Forecast + Control Year-To-Date.

This type of control allows us to anticipate the final result compared to the budget taking into account the Year-To-Date + justified forecasts until the end of the year.

In this model we incorporate forecasts that have an impact due to the actions that we plan and execute.

This system has a great advantage and it is that we can influence the final result to try to achieve the objective.

For example, we foresee that sales are a bit stagnant and if they do not increase, the objective will not be achieved as long as the gross margin is maintained and some items of structure costs are increased, but that allows exceeding the breakeven point for this growth.

Taking this into account, we can increase spending on commercial actions in order to boost sales, as long as we know the impact that actions will have on increasing sales and we know the cost of commercial actions.

Planning and executing actions on the forecasts taking into account the Year-To-Date result, we have a good chance of approaching or exceeding the set objective.

Otherwise, the only thing we can do is get a completely uncertain result, which can be positive or negative, we cannot influence it.

Are we interested in knowing where we want to go and putting the means to achieve it?

Who would not like it.

We tend to avoid uncertainty, we like to have everything under control, especially in financial matters.

What employee does not like to know what he is going to earn each month in order to plan its own finances.

In a company the risk is greater, so uncertainty should be reduced as much as possible.

And this is what budget control allows.

9 common mistakes in Budget Management

Recently, a frozen food company told me that they had tried to implement a budget on several occasions as a measure to redirect the situation of the company.

They had been with negative results for many years and they thought that the solution consisted in reducing the costs of raw materials, direct labor and overheads.

The many start-up attempts generated mistrust in the team, they considered that the tool contributed very little and wasting their time. The situation had demotivated staff for future management changes, even generating conflicts between different departments.

Analyzing the previous launch attempts, it was discovered that they had made some design mistakes.

1) They had not prepared the budget in line with the strategy and the Business Plan.

The strategy and the budget followed different paths, the strategy pursued growth, while the budget pursued cost reduction, in some cases the objectives contradicted each other. The budget is the economic translation of the strategy, so they must go linked.

2) They had not linked the accounting accounts with the activities and resources of the company.

They only took into account the accounting values for the preparation of the budget. They had not produced a detailed income and cost budget for calculating gross margin and net profitability. Ideally, you should have an accounting budget, a cost budget, and a revenue budget.

3) They had not made an action plan that would allow them to achieve the objectives.

They had objectives but no plan of what to do, who has to do it and when it has to be done.

4) They had not delegated the different items of the budget to those responsible for the area.

There was only one person responsible for the budget, both for the design, as well as for its execution and control, in this case the person in charge was the head of administration, the area managers were unaware of their objectives and consequently had no motivation to act.

5) They had not involved responsibles of the area in the preparation of the budget.

They did not ask the people who knew the most about the company’s activities, those who know what can and cannot be achieved, as well as being the people responsible for executing the action plan.

6) They had not considered the budget as an overall goal.

Budgeting involves working as a team to achieve a common goal, not individual goals assigned to each area without a joint goal.

7) They were unable to detect the causes of the deviations.

They did not know that it affected the achievement of the budget, consequently it was difficult to know where to improve.

8) They did not use the budget as an improvement tool.

They only considered the budget as a tool to reduce expenses, the budget control system could not correctly perform its function of improving competitiveness, improving profitability, detecting opportunities, eliminating waste….

9) They used the budget as a tool of pressure and control.

The use of the budget as a control tool generates demotivation, distrust and rejection among the staff, which made its acceptance and implementation even more difficult.

Errors in the design of budgeting and its management can generate more problems than advantages.

The budget is an essential tool if your company needs to be more competitive and improve continuously to achieve positive results in the Income Statement.

Advantages of implementing a Budgetary Control System with Projections in your company:

- Maximize PROFITS

- Improve internal processes to be more competitive

- Anticipate decisions to achieve desired results

- Encourage the entire organization to continuously improvement and not be left behind

- Delegate responsibilities and Evaluate the performance to Directors

More information about Controlling Excel Tools

- ROI Analysis How ODOO Makes Companies earn Money

- Hotels Excel Cost Calculation

- Excel spreadsheet Strategic Plan

- Project Management Excel Templates

- KPIs Management Excel Templates

- Decisions Sale Price Lists Calculation Free Excel Template

- Employee Absences Free Excel Template

- Management Accounting as a Control and Decision-Making Instrument

- Excel Template Employee Training Control

- RH Talent Box Grid Excel Template

- Payments Due Date Control Free Excel Template

- Projects Kanban Control Excel Template

- Inventory Control and Dashboard Excel Template

- Warehouse Inventory Control Free Excel spreadsheet

- How the Budget Control service works

- Actual Vs Budget Excel Templates

- Wedding Budget Control M1 Free Excel Template

- Travel Expenses Control M1 Free Excel Template

- Digital Marketing Dashboard Control M1 Free Excel Template

- How to forecast Purchase Orders with ODOO

- Marketing Budget Excel Spreadsheet

- Excel Templates Financial Dashboards Pack

More Videos about Management Accounting

![]()

Industrial company financial manager

Dani is helping us to use ODOO more efficiently, we are rapidly leveling up with the ERP. It is also preparing us very useful analysis and control reports and outstanding management tools. Always available by phone or email, willing to help and collaborate in everything that is proposed. Very professional and fast work. A key service for our company.

Controlling Consultant

Controller ODOO ERP

Email: dani@cashtrainers.com