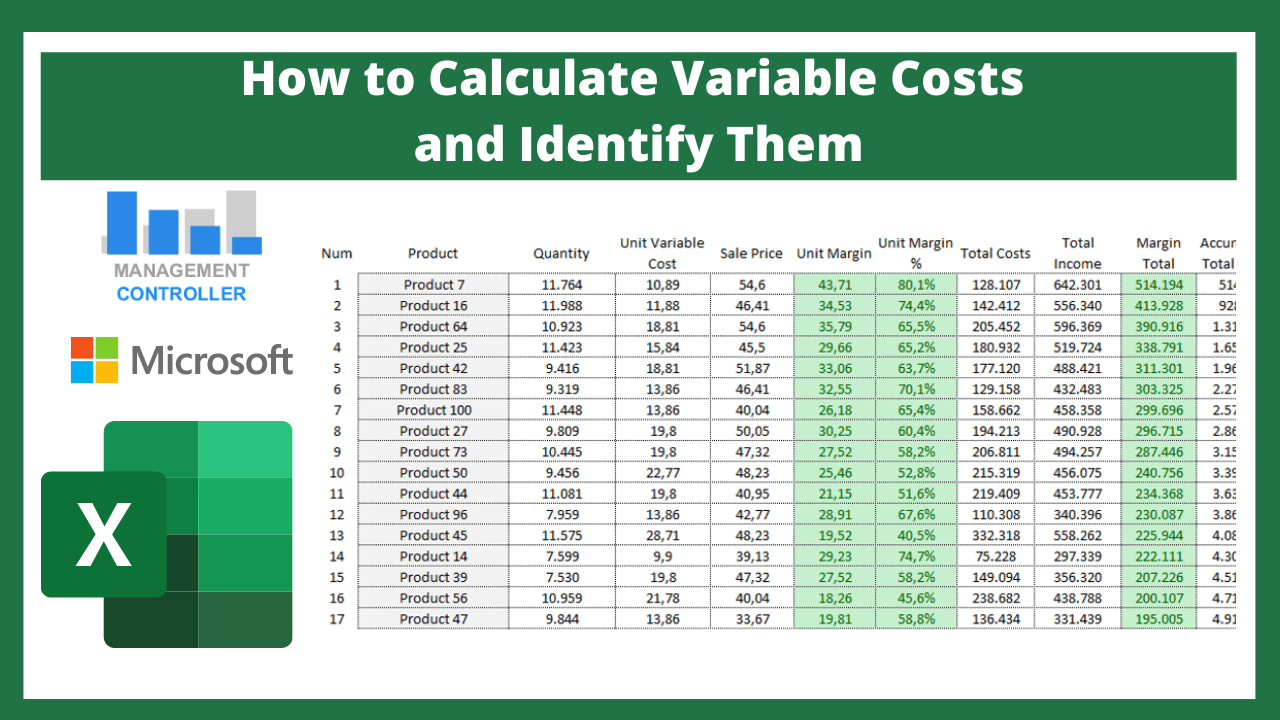

How to Calculate Variable Costs and Identify Them.

There is usually a lot of confusion regarding the type of costs, such as variable and fixed or direct or indirect.

Variable and fixed costs are a way of classifying costs according to their behavior, while direct or indirect costs are classified according to their ability to be assigned or associated with a cost object (product, service, project, cost center, machine, customer…)

When calculating costs we normally use direct and indirect costs, although in certain analyzes it may be interesting to perform a study on whether their behavior is variable, semi-variable or fixed.

The concept of variable cost in a very simple way would be that cost that you can leave out quickly and without additional costs.

The most variable cost in companies is the acquisition of materials for storage and distribution or raw materials for transformation in manufacturing processes.

If the company temporarily or completely reduces or ceases its activity, the first thing it does is stop buying materials and raw materials.

However, it cannot be detached from the rest of the costs so easily.

If a company temporarily ceases its activity, the cost of employees can be reduced but it does not disappear completely, which is why it is usually considered semi-variable. Maybe years ago it was more variable. But fortunately for the employees and not so much for the employer, if the workers have a contract, it is not so easy to get rid of their costs without incurring a significant additional cost. At least this is what happens in some countries.

Perhaps in other countries the cost of workforce may be completely variable.

For this reason, many companies opt for the formula of outsourcing services.

Instead of hiring staff to increase the workforce, companies that provide services or self-employed workers are opted for.

These types of costs are completely variable, so variable that there may also be a risk that the service company or self-employed person will stop providing the service for any reason.

If the company ceases its activity if there are no clauses in the contracts that prevent it, the company can quickly get rid of these costs without any significant additional cost.

Today many of the services we use work by subscription, that is, you no longer buy the product, but rather rent it. Such as certain software, mobile apps or popular streaming platforms.

These are examples of highly variable costs. If, for example, you go out in holydays for a month and you are not going to consume the streaming platform, you can unsubscribe and re-register when you return. You control the cost.

But it may be the case that you turn a variable cost into a fixed one, and this is a consequence of the use you make of the service or its consumption.

For example, paying an annual gym fee and never going. Or pay the annual fee for a streaming platform and never use it.

These cases are costs that in a short time you realize that you do not need, but you cannot get rid of them until the end of the period you have paid. Therefore, what at first seems variable actually becomes a fixed cost for a given period of time.

These simple examples are also common in companies, such as unnecessary investments, hiring staff they don’t need, excess stock of materials or raw materials, hiring services they never use…

The non-use or consumption of a resource that has involved a cost that you cannot easily get rid of can be converted into fixed costs.

This means that if you temporarily close the company these costs will continue to be incurred.

How can it be that a cost as variable as that of materials or raw materials can become a fixed cost?

Imagine that you manufacture a product that consumes a raw material, as the forecasts are optimistic, you acquire the volume of consumption for 2 years of this raw material to take advantage of discounts for rappels and early payment.

Shortly after having acquired, received and paid for the raw materials for 2 years of production, the market turns around and stops demanding the product you are going to manufacture.

It is a raw material that you cannot use in another process and the supplier does not accept returns unless the product is defective.

You can try to resell them to other companies, but they don’t need as much volume and they already buy what they need from their usual supplier.

Possibly you can resell them at a price much lower than the cost, which will mean an additional cost for which you will not obtain any margin.

Therefore, the raw material is no longer variable, behaving as a fixed cost for at least 2 years.

As I have commented previously, the usual calculation of budgeted or forecast costs or for real margins is the use of the classification criteria according to the capacity of assignment or association to the cost objects, which would be the direct or indirect costs.

A direct cost is usually variable or semi-variable, and indirect costs can be variable, semi-variable or fixed.

The analysis according to its variable or fixed behavior is usually used to make decisions regarding to vary or not to vary key costs. For example, are we interested in having our own staff, which would entail a semi-variable or fixed cost, or do we outsource the process and make it completely variable?

Another example, the analysis when purchasing a server for computer applications that entails a fixed cost for the company, such as depreciation, maintenance, electricity consumption, or an external server is chosen with a monthly cost without the need to take an investment and therefore we do not have the cost of depreciation, or electricity consumption, or maintenance, in addition to including constant updates and improvements, so we would not need to constantly renew it, as it may be the case with our own server… In addition, in the case of cessation of activity or if we no longer need the server we can easily leave out the cost.

The same applies to the acquisition or rental of vehicles or machinery.

The purchase of a vehicle requires an investment involving depreciation costs, insurance, maintenance, breakdowns and loss of value from the time of purchase. A fixed cost until it is resold at a price much lower than its cost (initial investment, insurance, maintenance, breakdowns…). However, if you opt for the rental option, the cost is semi-fixed or semi-variable, since the cost is a monthly fee for a certain period of time, but once that period of the contract has ended, you can decide whether to continue with the service or abandon it.

Therefore, the variability of costs is something relative that allows the company to make decisions according to what benefits it most.

There are companies that choose to vary everything they can, in this way they can reduce or increase costs depending on sales volumes.

While other companies avoid outsourcing and variable costs, this type of company has a great attachment to ownership, that is, they need to assume the costs as their own despite the risk of having high fixed costs, which reduces flexibility in the face of variability of sales volumes or market demand. Usually, these companies suffer when demand falls, and costs cannot be easily break away.

We have seen this in many businesses in the unfortunate pandemic that we have all experienced. Those businesses that have had to temporarily cease their activity have had to take on all the fixed costs they had despite having a very low sales volume or a non-existent sales volume.

Those companies whose costs were much more variable may have suffered to a minor effect, since they have been able to temporarily get rid of them.

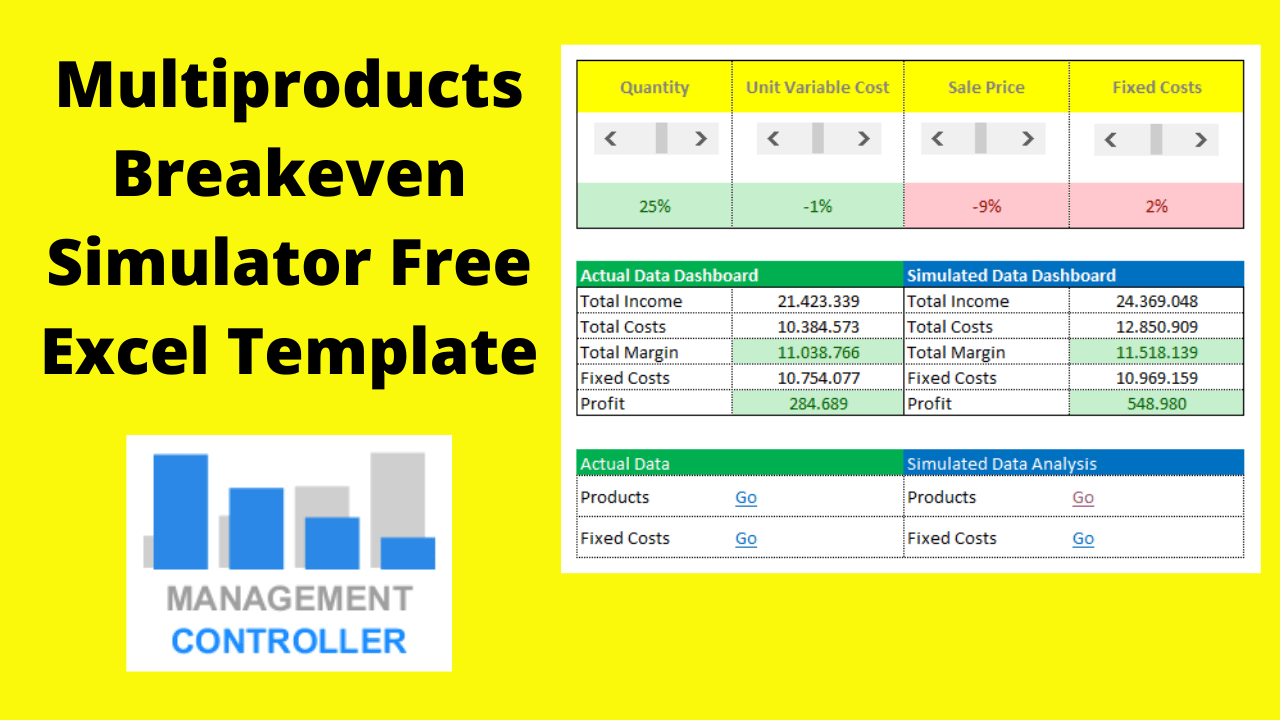

The analysis of variable and fixed costs is often useful to calculate the break-even point, the point at which the company begins to make a profit, since margins obtained from viable costs are higher than fix costs.

If you are interested in a practical application for calculating variable and fixed costs, here is a free tool for calculating “Break-Even Point Multiproduct Free Excel Template”

More information about Controlling Excel Tools

- Inventory Control and Dashboard Excel Template

- Budget Control Excel Year-to-Date & Full-Year Forecast M11

- Wedding Budget Control M1 Free Excel Template

- How to forecast Purchase Orders with ODOO

- What is Budgetary Control?

- Training Management Free Excel Spreadsheet

- Budget Control for Events M1 Excel Template

- Excel Template Financial KPIs Dashboard

- Employees Best Practices Improvements Requests M2 Free Excel Template

- Excel Manufacturing Standard Costs and Margins M10

- Excel Template Action Plan PRO

- Customer Invoices Free Excel Template

- Employee Recruitment Excel Template

- Personal Finance Free Excel Template

- Budgetary control System with Projections example

- How to Calculate Variable Costs and Identify Them

- Balanced Scorecard M1 Excel Template

- Digital Marketing Dashboard Control M1 Free Excel Template

- Excel Template Accounts Payable Control

- New Investments Requests Form Free Excel spreadsheet

- Excel Templates Financial Dashboards Pack

- Timesheet Excel Template PRO

More Videos about Management Accounting

![]()

Industrial company financial manager

Dani is helping us to use ODOO more efficiently, we are rapidly leveling up with the ERP. It is also preparing us very useful analysis and control reports and outstanding management tools. Always available by phone or email, willing to help and collaborate in everything that is proposed. Very professional and fast work. A key service for our company.

Controlling Consultant

Controller ODOO ERP

Email: dani@cashtrainers.com