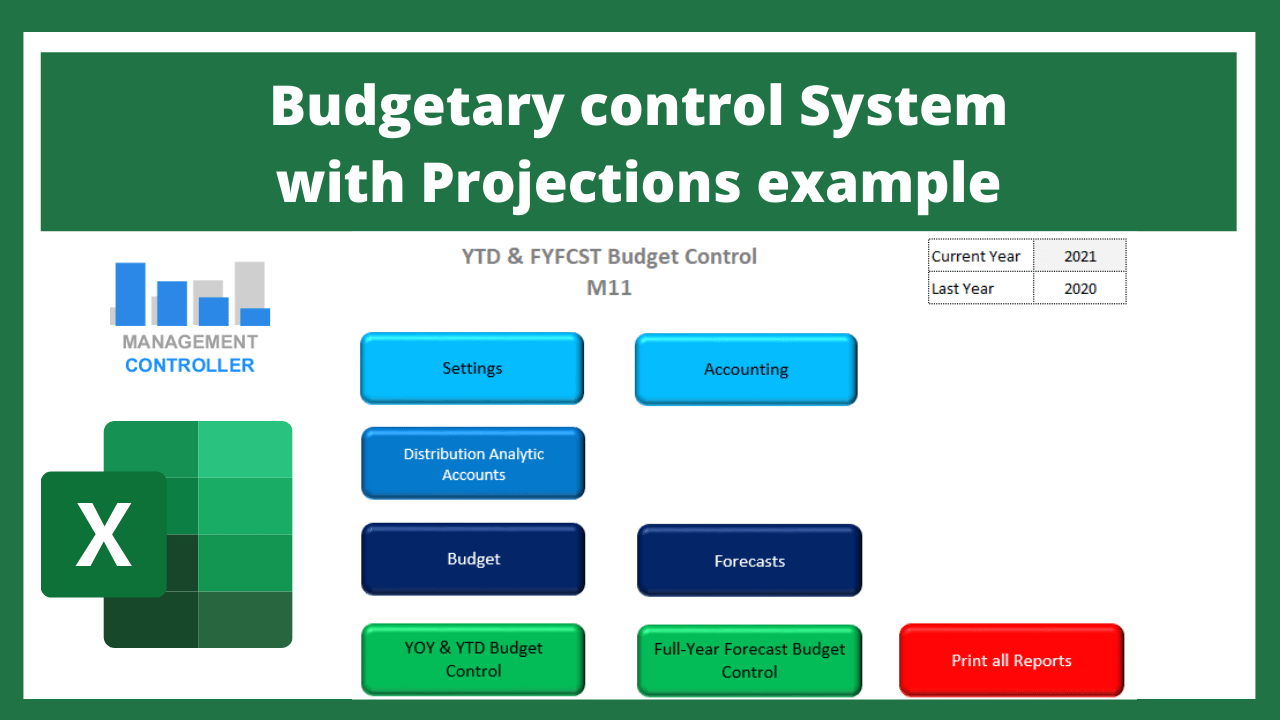

Budgetary control System with Projections example.

Recently, the company WoodBeauty Ltd. (fictitious company name to preserve confidentiality) implemented the classic accounting budget based on adjustments over the previous year.

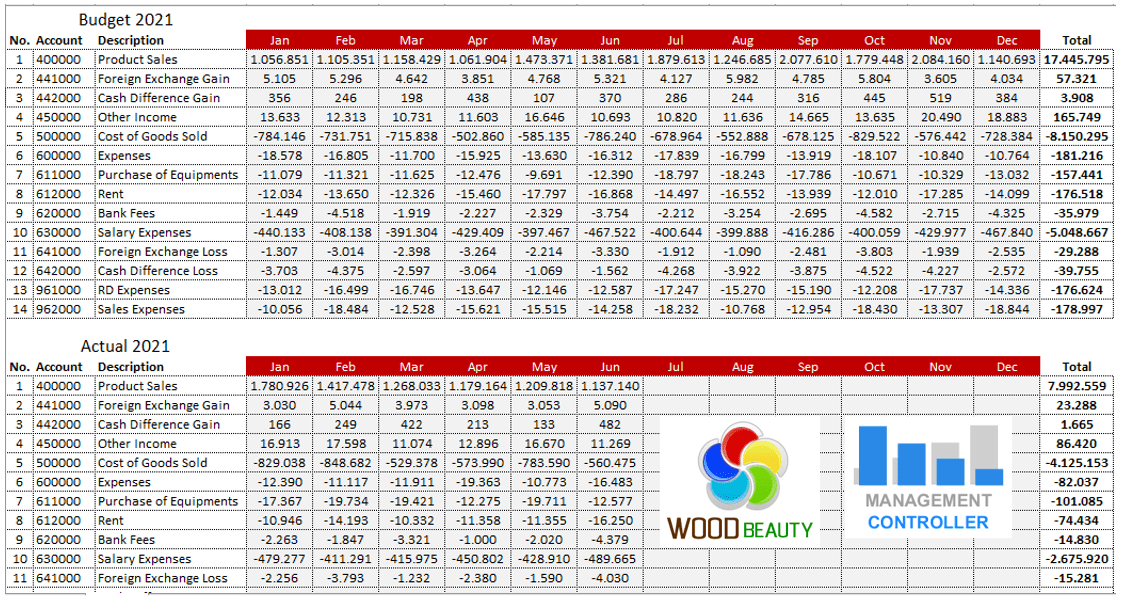

The budget had a structure similar to the one presented in the following image. A simple system that allowed you to compare your actual income and expenses with your budgeted ones.

This basic system provided the company with a posterior view (the accounting for the month already closed) on the difference between the desired economic result (budget) and the actual one.

The following month they performed the same process and so on until the end of the year.

Once the financial year was closed, an annual comparison was carried out.

If the objectives had been achieved the Manager was happy and if they were not achieved, what will he do? Maybe next year they would be luckier in getting them.

With this system, they never had any control over the budget. The final result was unpredictable.

Why didn’t they have control over the budget?

In the first place, if you analyze the information a posteriori you cannot act or make decisions on it, what is done is done.

If a budget is established (desired situation) aligned with the strategic objectives, an action plan to try to achieve it is recommended, otherwise it is impossible to know what to do to fulfill the results.

How do we know if we are going to reach the budget or not?

Very simple, through the forecasts.

But isn’t forecasting the same as budget?

Forecasts are situations that we believe will occur while the budget is the desired situation that we want to achieve, normally aligned with strategic objectives

It is not the same to wish for something as to think what is really going to happen.

The good thing about working with forecasts is that these economic events have not yet occurred, therefore if they have not occurred, we can act on them to change, alter and modify them through actions and decisions.

Let’s imagine that before starting year 2021 we have a budget for the personnel item of 100,000 Euros.

However, forecasts indicate that at the end of the year the cost will be 120,000 Euros.

Then we have a whole year ahead to try to get the actual cost to be 100,000 or less instead of the expected 120,000.

To get this, actions are established to try to achieve that objective.

And this is the most complicated part, “taking actions” or “making decisions.”

With the expected workload, the personnel needs are 120,000, but if we make improvements in internal processes, if we optimize work times, if we carry out automations, possibly the personnel needs can be reduced.

In a company everything is linked, possibly to reduce the needs of personnel it is necessary to invest, but if this investment not only reduces personnel costs, maybe also improves production capacity, reducing the cost of the manufactured product.

Then we would have a greater margin, we could reduce delivery times, improve margins and cash flow, reduce financial costs …

It is like the domino effect; the movement of a piece makes the rest of the pieces move as well.

For this reason, action plans have to be well prepared and constantly monitored.

So the budget only has to be compared against the forecasts to be effective?

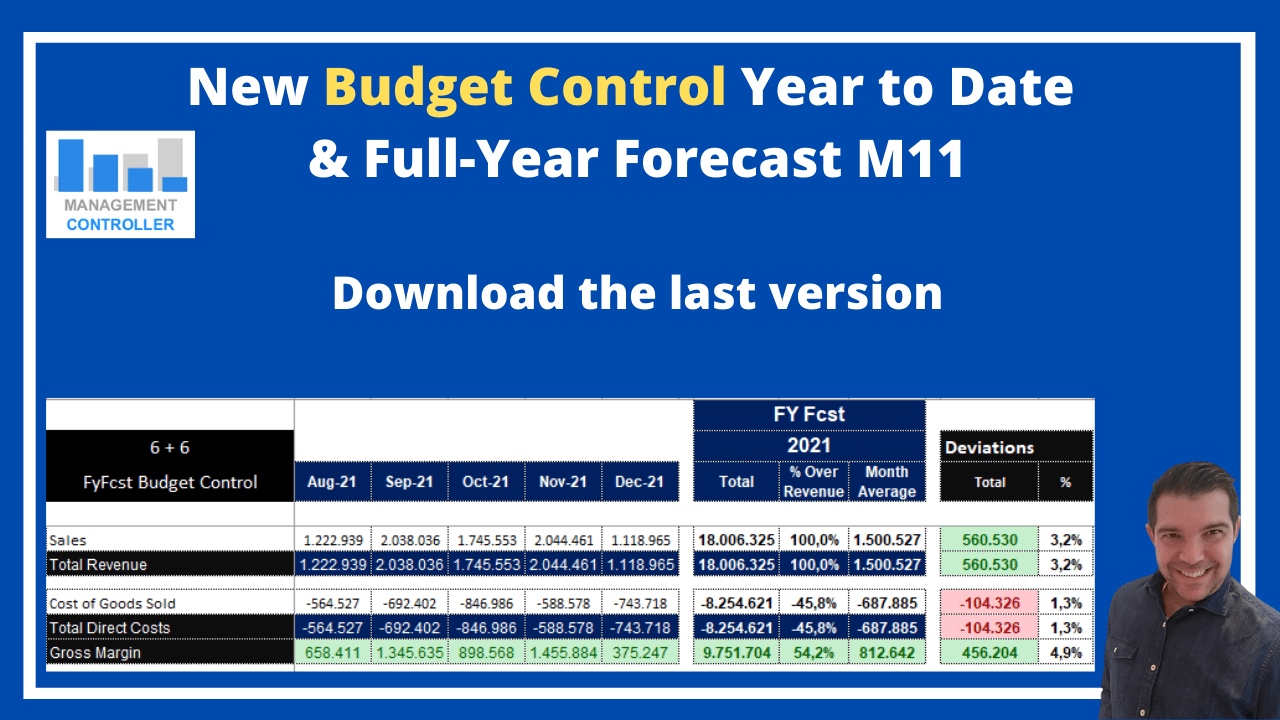

It depends on the time of year that we are analyzing. If we already have the first month of the year closed, we have fantastic information that is 1 actual month and 11 months of forecasts, when the second month closes, we will have 2 months with actual information and 10 months of forecasts.

The good thing about this system is that as the months close, the forecasts can be adjusted. We already have started working on the action plan, the action plan can be adjusted as forecasts change, also action plans performed can affect the forecasts. Then we can say that action plan and forecasts are tightly linked.

If we constantly monitor the action plan, its evolution, adapt it as the situation changes and adjust the forecasts, then we have a good chance of reaching the desired situation (the budget)

And this is what the owner, manager or area managers are after, right?

The company WoodBeauty Ltd. changed its budgeting system last year and since then it has greater control over the budget, working with forecasts and an action plan allows it to make internal improvements, which have a great impact on the results of the company.

Its results are improving, making it a more competitive company and it is already looking at future expansion and growth.

Press here to check out the budgetary system than implemented WoodBeauty Ltd.

Keeping a budget control in the company adjusting forecasts, is it really that important?

It is a pity that we do not have unlimited resources to live, without having to worry about what we spend or invest our money on.

In a family economy we know that the money that comes in on a monthly basis so we can make a forecast of what will come in next year.

Based on the expected inflow of money, we can make decisions for items of money that we can spend on housing, food, transportation, education, clothing, leisure, savings and investments….

The income and expenses budget is the desired situation, but reality can generate deviations from what is desired, so based on the realities we adjust the forecasts to try to achieve what is desired.

If, for example, one month we have an extraordinary expense not contemplated in the budget, we can adjust the forecast by reducing in other items so as not to deviate from the budget.

More or less this is what family economies usually do, some will do mind calculations, others more meticulous will do it on paper and the more detailed ones may carry a spreadsheet with all the numbers.

If in a family economy it is essential to keep a budget control and make corrections in the forecasts to avoid a negative deviation of the budget.

In a company it seems obvious that a control of these characteristics should be kept, and even more so with the number of factors that affect the result of the company, but the reality is that very few companies have a budget control system adjusting the forecasts to avoid a deviation from what was budgeted.

Companies that keep a budget only compare what is real with what is budgeted, but do not take into account the adjusted forecasts for the next few months.

For example, reduced sales prices, fall in demand due to some factor, increased costs of raw materials, increased energy prices …

We may know what will happen in the coming months until the end of the budget year, but we do not include the forecasts in the system to analyze the final result of the months with actual data, also including the months with forecast data to compare it with the full-year budget and determine if the desired situation will or will not be achieved.

If we know what is going to happen, we can take actions to correct the forecasts and achieve the budget.

Advantages of implementing a Budgetary Control System with Projections in your company:

- Maximize PROFITS

- Improve internal processes to be more competitive

- Anticipate decisions to achieve desired results

- Encourage the entire organization to continuously improvement and not be left behind

- Delegate responsibilities and Evaluate the performance to Directors

More information about Controlling Excel Tools

- Human Resources HR Budget Excel Template

- Excel Spreadsheet for SWOT Analysis

- Tracking Shipments Excel Template

- Pipeline CRM Excel spreadsheet

- E-Commerce KPIs Control Excel Template

- Timesheet Control and Report Free Excel Template

- Documents Management Free Excel Template M1

- KPIs Management Excel Templates

- RH Talent Box Grid Excel Template

- Payments Forecast Control FREE Excel Template

- Excel Template for Performing a Net Worth Analysis

- Projects Control with Tasks Free Excel Template

- Does a company need to automate or optimize administrative tasks?

- What is Contract Management Excel Template and download a spreadsheet

- Working Hours Timesheet Free Excel Template

- Download Example of Excel thermometer chart

- Excel Template Action Plan PRO

- Financial Plan M3 Free Excel Template

- How to use an organizational chart KPI Excel template to improve your business performance

- How to forecast Purchase Orders with ODOO

- Bugs Tickets Resolutions Control Excel Template

- Advantage cost calculation with Excel in companies

More Videos about Management Accounting

![]()

Industrial company financial manager

Dani is helping us to use ODOO more efficiently, we are rapidly leveling up with the ERP. It is also preparing us very useful analysis and control reports and outstanding management tools. Always available by phone or email, willing to help and collaborate in everything that is proposed. Very professional and fast work. A key service for our company.

Controlling Consultant

Controller ODOO ERP

Email: dani@cashtrainers.com